May 2020

MIXED MESSAGES

By the end of May, the majority of investors believe the worst of the COVID-19 economic shutdown is behind us. The S&P/TSX Composite was up 4.2% in the month, representing a return of over 35% since the low reached on March 23rd. The S&P 500 was up nearly 7%, roughly 38% from Year-to-Date lows. The rally is being fueled by a mixture of exuberance from the possible development of a vaccine and optimism that the worst of the economic damage is behind us as lockdown measures begin to lift.

Although the stock market is forward-looking and an indicator of investor sentiment, we struggle to reconcile these returns with what we’re monitoring in the data from indicators. First off, when measuring the strength of a stock market rally we look at its breadth to see whether it encompasses the broad market or a select few. Currently, a handful of companies account for over 25% of the S&P 500 as these stocks hit new all-time highs while the rest of the index has experienced more meagre returns.

Looking to the ‘goods’ sectors of the economy, a broadly used indicator is the Purchasing Manager’s Index (PMI), which measures the monthly variation of business activity from a selected group of manufacturers across the country. A reading of 50 means economic activity is flat, while above 50 means growth and below means contraction. In April, Canada’s PMI hit a record low of 33 meaning significant contraction. In May, that number is up to 40, which still shows contraction but at a lesser pace.

We are cautious on the scope of the economic recovery and the impact from inflation. With a massive amount of consumption pulled from the market and rampant unemployment, we are experiencing disinflation where prices for consumer goods drop over the measured period. As we move out from the shutdowns and while central banks are printing money and pumping stimulus into the economy and governments continue to provide significant fiscal stimulus, we run the risk of runaway inflation or even stagflation, a scenario where inflation is rising concurrently with high unemployment.

All this to say, we have been diligent in monitoring financial markets and economic indicators. We have been re-evaluating our model positions in light of new circumstances and information to ensure we are positioned in a way to reduce the impact of another market sell-off while also remaining positioned to take advantage of a further rally.

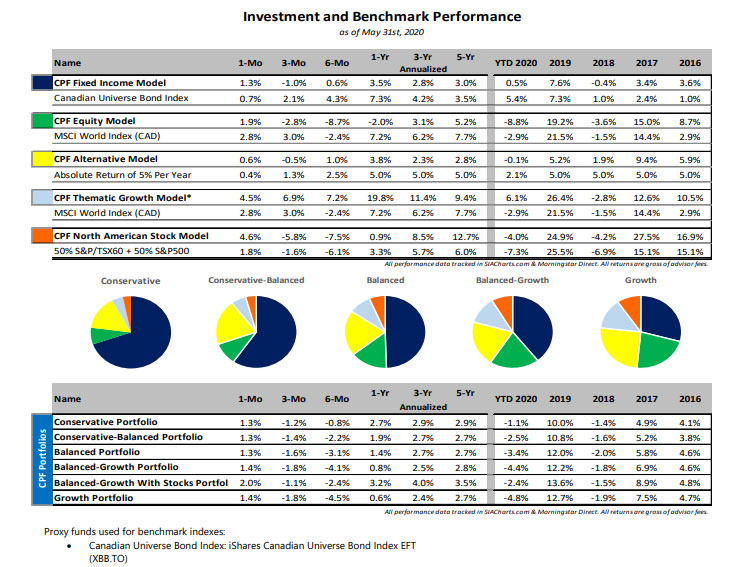

Portfolio Contributors

- Our equity exposure to cyclical sectors like Consumer Discretionary and Technology added significantly to portfolio returns

- Asset-backed fixed income securities held within PIMCO Monthly Income made the fund our top performing fixed income position

Portfolio Detractors

- Our investment in international real estate brokerage, Colliers International Group, slumped after missing earnings estimates

- The long duration of Vanguard Aggregate Bond ETF was flat for the month, as investors shifted to a risk-on sentiment

- http://performance.morningstar.com/Performance/index-c/performance-return.action?t=SPX

- https://www.ccn.com/stock-market-warning-6-mega-stocks-dominate-sp-500s-21-4-trillion-cap/