January 2020

Start of Tumultuous Twenties

One century ago, in January 1920, the League of Nations was officially inaugurated following the Treaty of Versailles, providing a forum for resolving international disputes. This was the foundation for the organization we now know as the United Nations. Since then, international collaboration has allowed countries to flourish through globalization and the resulting trade synergies. One hundred years later, we continue to see the effects of this cooperation in headlines around the world.

Representatives from the US and China signed a Phase One trade deal, the basis of which was an increase in purchases of US goods over a two-year period. The effects of the trade deal are expected to be delayed given the outbreak of the Novel Coronavirus, which has infected more than 20,000 people in China so far. Quick action taken by governments around the world has limited the spread of the virus, although we still expect to see an impact to global growth in the first quarter of 2020.

North American markets had a slight pullback before regaining lost ground as investors shifted to a risk-off sentiment until more information was known about the virus. When it became clearer that 2019-nCoV was less lethal and contagious than similar outbreaks of SARS and MERS, investors used the opportunity to ‘buy the dip’ in equity markets. Although equities have rebounded, reduced global consumption has affected energy markets with WTI Crude trading down over $10 per barrel since the start of the year. The Loonie, reflecting this sell-off in crude markets, depreciated over 1.50% against the US dollar.

Leaders from both public and private sectors gathered at the 50th anniversary of the World Economic Forum, commonly referred to as Davos after the Swiss town where the event is hosted. The conference spanned topics from the global economy and climate change to genetics and cybersecurity. Key takeaways from the event was a focus of C-suite executives on climate risk and a generally optimistic outlook on international growth.

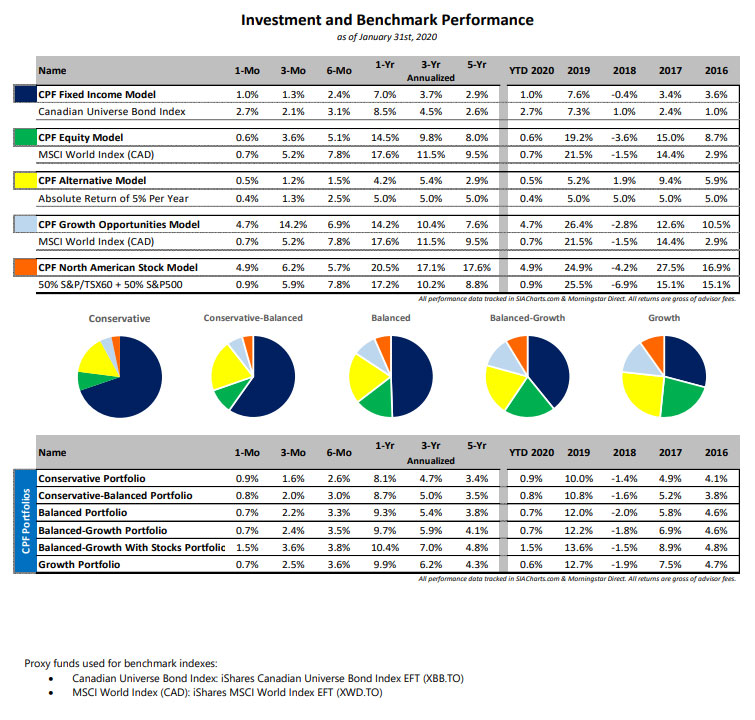

Portfolio Contributors

- Nearly all positions in our Canadian equity portfolio outperformed their benchmark, continuing the outperformance the submodel exhibited in 2019

- Our positioning in Low Volatility US companies benefited the portfolio during the sell-off, with iShares Edge MSCI Min Vol USA ETF outperforming the benchmark by nearly 2.5%

Portfolio Detractors

- EdgePoint Global Portfolio slightly underperformed due to their overweight exposure to Japanese equities. This region is experiencing a larger drawdown due to the 2019-nCoV scare

- CC&L Global Market Neutral detracted largely from the performance of our Alternative weighting. Our team had a meeting with CC&L’s Quantitative Management team and the product is currently under review by our Investment Committee

All performance numbers sourced from Morningstar Direct.

Special Report

Advisor Year Ahead Conference Update

The Advisory Team recently attended the 14th annual iA Securities Year Ahead Investment Conference in Toronto featuring some of the top investment minds from both within and outside our organization.

The purpose of the event was to help attendees get a better sense of what we should be expecting from financial markets in 2020 by showcasing the differing viewpoints of more than 20 industry experts. The day featured some impressive talent, including iA Financial Group’s Chief Economist, Clément Gignac, Chief Investment Strategist at Dynamic Fund, Myles Zyblock, and Alfred Murata of PIMCO, who runs the largest mutual fund in the world. Things were capped off by Greg Valliere, the Chief U.S. Policy Strategist at AGF Investments. Greg broke down the political landscape and the ramifications for stocks and bonds as we proceed towards November’s U.S. elections.

Some key takeaways of the day included:

- Despite being 11 years into the longest economic expansion ever, global growth may be ramping up and some of the storm clouds that impacted 2019 have dissipated. While there are few areas within the market that can be classified as outright bargains, what we’re hearing is that renewed economic growth should be supportive of asset prices.

- The growth won’t be so pronounced as to run the risk of causing things to overheat. This should keep central banks on the sidelines. In a way, one could call this a Goldilocks environment.

- The past number of years have shown that if the economic cycle holds together, it has paid not to get too pessimistic. There is not much of an expectation that things will fall apart this year, so staying the course seems to be the wise approach. The U.S. election will be a regular part of the news cycle for much of this year, but any impact on the stock market will likely be short lived. Further, the election is Trump’s to lose, and look for him to pull out all the stops to secure his victory, including another round of tax cuts.

Bragging Rights

Brent and Gary were honoured to open the Toronto Stock Market on Tuesday, January 21st. They joined BMO ETF’s as they launched their new ESG (Environment-Social-Governance) filtered ETF’s.