December 2019

2019 Wrap Up

Whether assisted by a Santa Clause Rally or the announcement of a Phase 1 trade deal, the S&P 500 finished 2019 up 30% (total return in local currency), an impressive feat for a “late cycle” market. The annual returns were spurred on by low interest rates, which allow companies to finance leverage at lower costs and push some investors to chase returns in equity yields rather than fixed income. The annual return was aided by the market selloff in the last quarter of 2018 in response to actions by the Federal Reserve, which provided a lower starting point for the following year. If we zoom out to compare against the highs of 2018, the index only returned slightly above 10% over that period, which is more closely aligned with the average annualized return for the index over the last 90 years.

The utility sector rallied in the United Kingdom as nationalization fears subsided after the Conservative Party led by Boris Johnson achieved a wide majority in the elections held on December 12th. The majority will remove some of the impediments the party faced when governing as a minority and clears the way for the UK to pass a European Union withdrawal bill, otherwise known as Brexit. The ability to pass a withdrawal bill removes the immediate threat of the UK crashing out of the EU without a deal, a scenario that would have harsh implications for businesses operating within the UK economy.

The Loonie started to rally against the US dollar over the month as global markets transitioned into a ‘risk-on’ mode. As we have discussed in the past, the dollar parity is largely impacted by the difference in central bank policy rates between the Bank of Canada and the Federal Reserve as well as crude oil prices. Whether this trend continues will depend on global geopolitical developments and the strength of the Canadian economy. If economic indicators begin to weaken in Canada, one of Stephen Poloz’s last moves as Governor of the Bank of Canada may be a rate cut, which would give up some of the appreciation the Loonie has seen.

Contributors

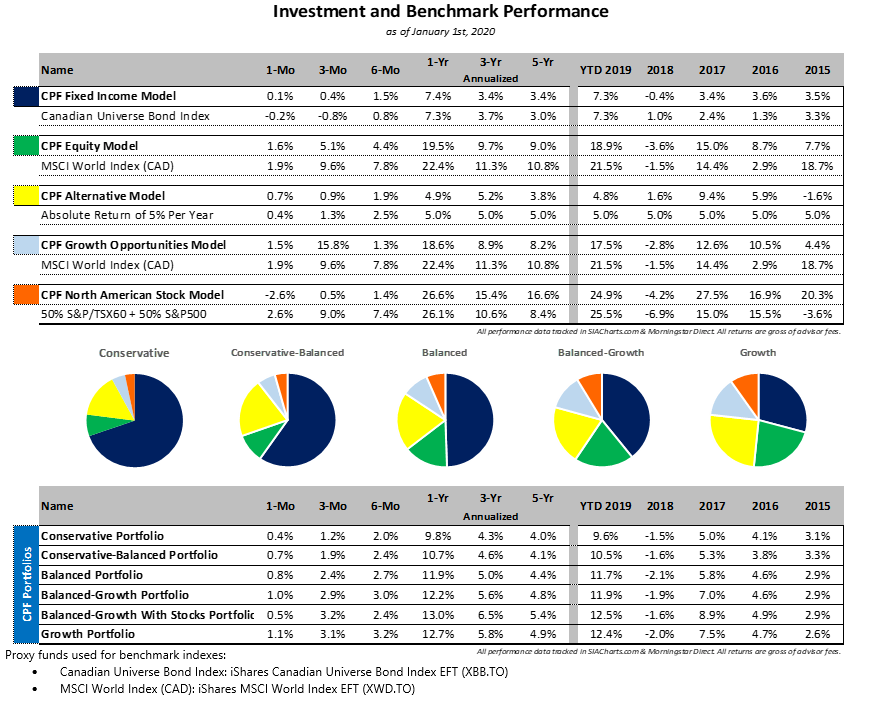

- Our selection of actively managed fixed income funds outperformed the benchmark, providing stability to the asset allocation

- Exposure to global infrastructure and agriculture generated returns above the S&P 500 (CAD-hedged) as these sectors rallied on the announcement of the Phase 1 trade deal

Detractors

- Some of our growth-oriented stock positions, Dollarama and Colliers International, declined after missing earnings estimates or after management revised outlooks for fiscal 2020

- Our underweight allocation to Canadian equity slightly detracted from performance as total return on the S&P/TSX came in below U.S. and EAFE markets

All performance numbers sourced from Morningstar Direct.